FY25 Audited Financial Results

31 July 2025

NARF INDUSTRIES PLC

Audited Financial Results

For the 12-month period ended 31 March 2025

Narf Industries plc (LSE: NARF), a leading U.S.-based cybersecurity group specialising in advanced threat intelligence and software system security, is pleased to announce its Audited Financial Results for the year-ended 31 March 2025. The Report is available in full on the Company's website at https://narfgroup.com/investor-relations/corporate-document.

Overview

- Strategic priority shifted to a scalable Software-as-a-Service (SaaS) model launching Ranger.ai, an Agentic AI threat and remediation platform for securing Open Source Software.

- US federal budget delays early in the period and subsequent DOGE disruptions resulted in a 50% annualized revenue decline.

- Costs were tightly managed and other significant contract wins, including its largest-ever $6.8 million INGOTS award, enabled the Company to advance within its financial resources.

- Strong foundation going forward, no need for new capital to execute core plans, and clear path to growth.

Executive Chairman's Statement

I am pleased to present the audited financial results for Narf Industries PLC for the year ended 31 March 2025.

The past year marked a significant strategic transition for the Group. For several years, we had been advancing cutting-edge government research and development ("R&D") work under our Social Cyber initiative - applying behavioural analytics and Agentic AI to secure open-source software ("OSS"). Then, in March 2024, the discovery of a backdoor in XZ Utils, a compression utility embedded in major Linux distributions, exposed just how vulnerable critical open-source infrastructure had become. That event brought urgency and clarity. We made the decision to shift resources and leadership focus toward rapidly transforming our Social Cyber R&D into a productised platform, now launched as Ranger.ai.

While Ranger.ai formally launched after the year end, its foundation was laid during the reporting period through intensive technical and product preparation. Ranger.ai represents a first-of-its-kind approach to open-source software security, combining behavioural analytics and an Agentic AI framework to expose vulnerabilities that traditional scanning tools often miss.

More than a technical milestone, Ranger.ai marks our first major step toward a scalable Software-as-a-Service (SaaS) business model - transitioning project-based R&D to build a recurring revenue foundation capable of supporting long-term growth. Early traction with government customers is already validating both the opportunity and the Group's strategic priority.

This shift in priority, however, coincided with external headwinds. U.S. federal budget delays and broader agency disruptions, like Department of Government Efficiency ("DOGE") intervention, materially impacted revenue, particularly in our Government Services and Solutions ("GS&S") segment.

Despite these challenges, we advanced the business by tightly managing cost and securing critical follow-on research contracts enabling us to execute our strategy with existing financial resources during the period.

Our GR&D business continues to reflect our ability to deliver frontier cybersecurity capabilities with a direct path to operational use. The $1.3 million U.S. Air Force contract for AI-powered Social Cyber Solution, announced in August 2024, marked a major milestone to transition project-based work to a more scalable SaaS model. The $6.8 million DARPA INGOTS win in January 2025, represented both a major technical milestone and the largest-ever contract in the Group's history.

Looking ahead, we expect GS&S will grow as its the primary delivery engine for our Ranger.ai platform to U.S. government customers. This involves early-stage deployments and building capacity to scale implementations across a close-knit network of agencies and their prime contractors. Commercial adoption is expected to follow, with efforts focused on partnerships and joint ventures to access broader market expansion.

The Board remains committed to executing this strategy with discipline. We entered the current period with a strong technical foundation, operational clarity, and the confidence that the decisions made over the past year will begin to yield visible, durable results. The Company's current contract pipeline and prudent cash flow management provides sufficient runway to execute our strategy through the current financial year, without reliance on new capital resources or significant near-term contract wins.

We remain confident that the intersection of our deep government expertise, technical excellence, and R&D transition to operational mission vision uniquely positions Narf for long-term value creation. Ranger.ai is a clear example of strategy in action - a cutting-edge cyber security product built to tackle some of the most urgent and complex challenges our customers face. As we prepare for broader rollout of Ranger.ai, we're encouraged by the early traction and exciting about the growth potential it represents.

John Herring

Executive Chairman

For further information visit www.narfgroup.com or contact:

Narf Industries plc

John Herring

Joint Broker

Tennyson Securities plc

Peter Krens

Tel: +44 (0)207 186 9030

Financial PR, UK

St Brides Partners

Paul Dulieu

Isabel de Salis

NARF INDUSTRIES PLC

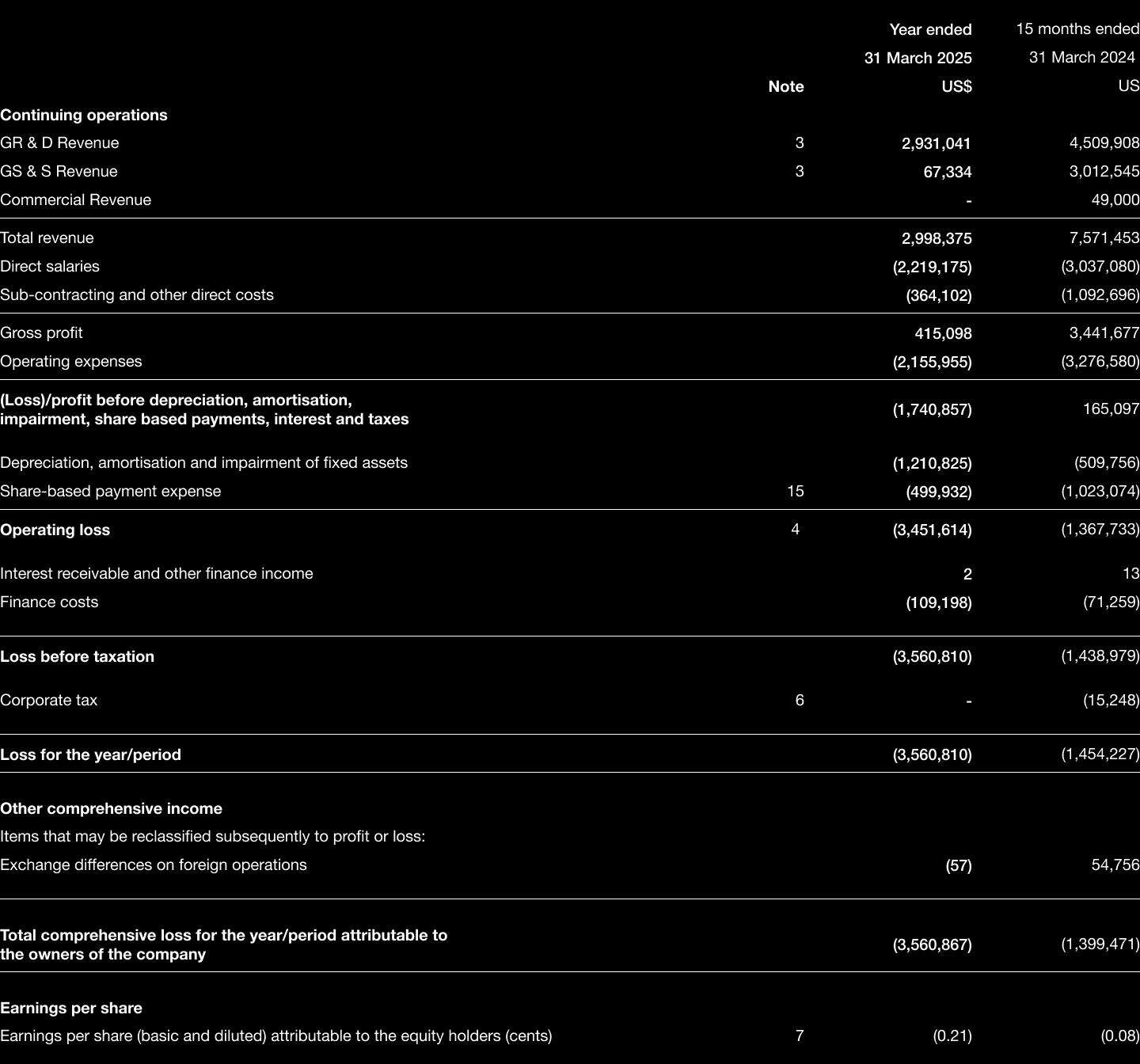

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 MARCH 2025

NARF INDUSTRIES PLC

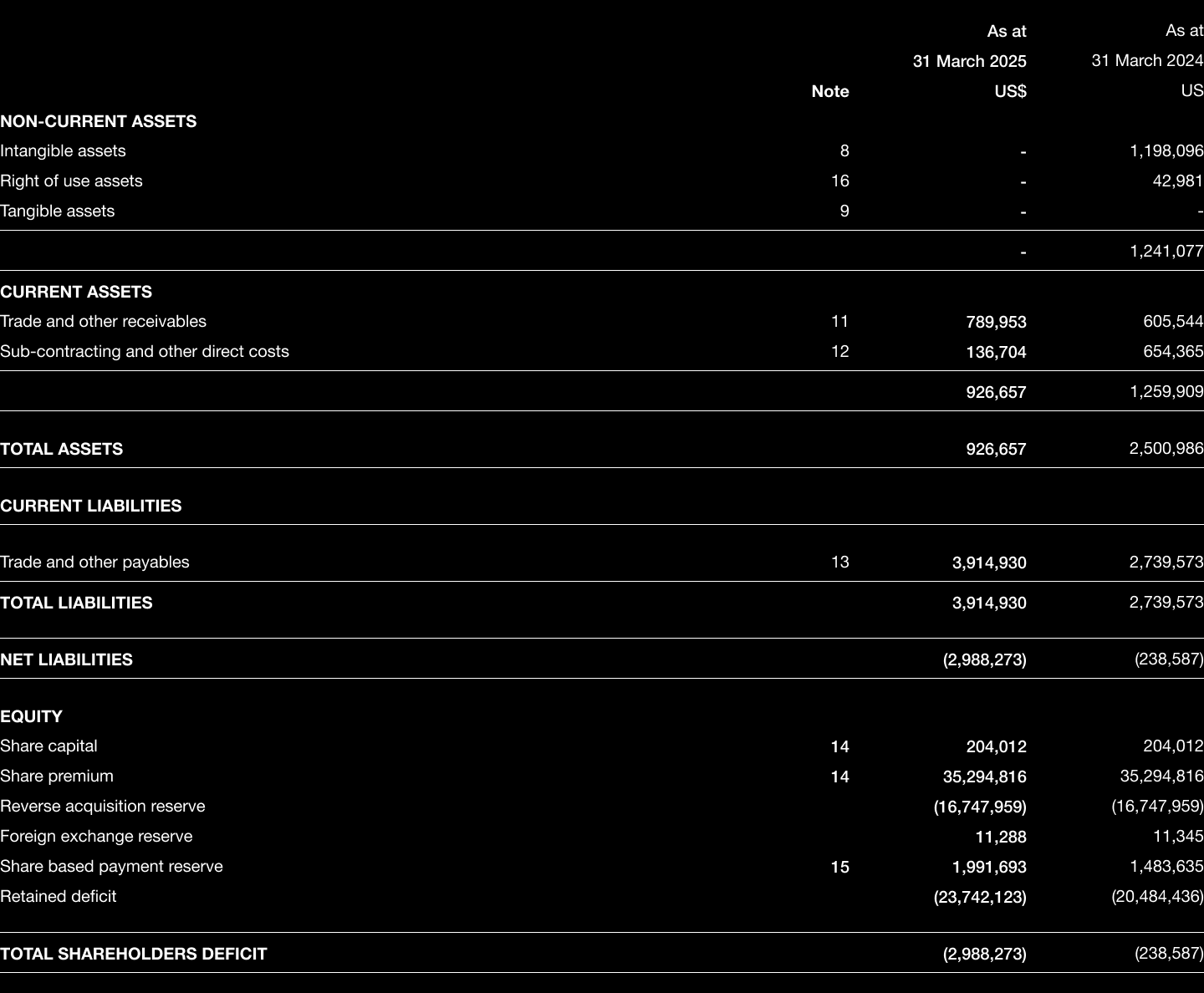

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS AT 31 MARCH 2025

NARF INDUSTRIES PLC

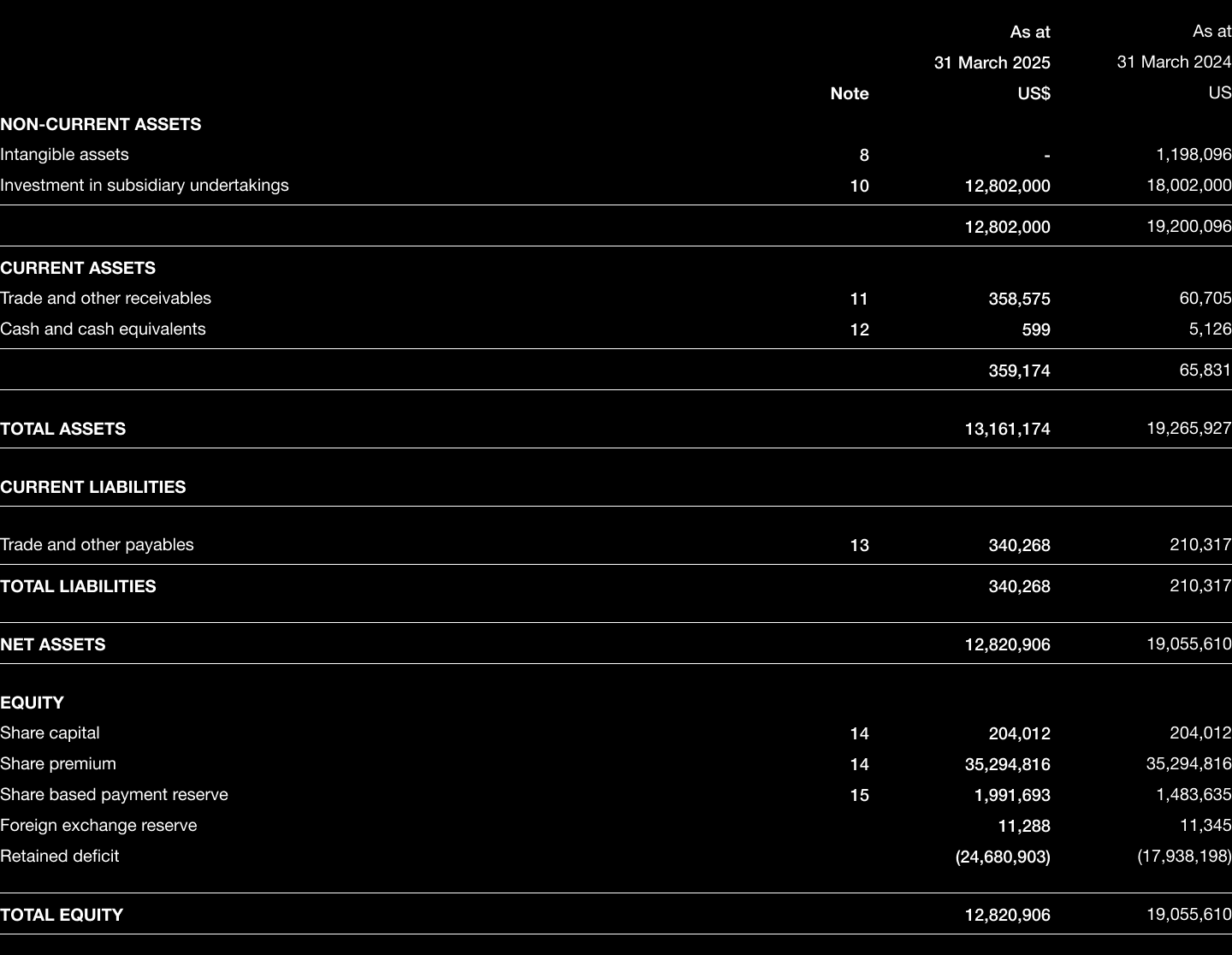

PARENT COMPANY STATEMENT OF FINANCIAL POSITION

AS AT 31 MARCH 2025

NARF INDUSTRIES PLC

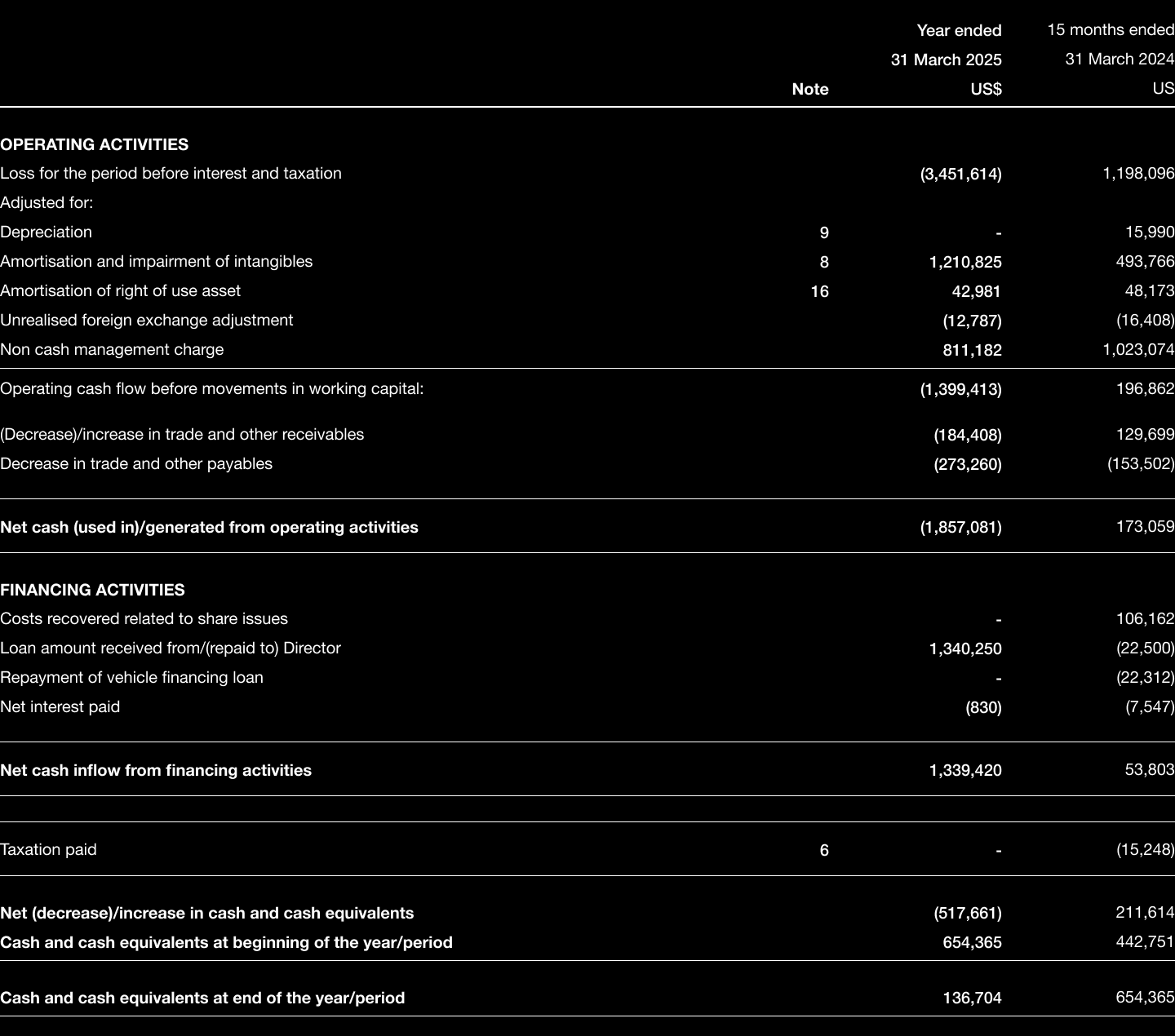

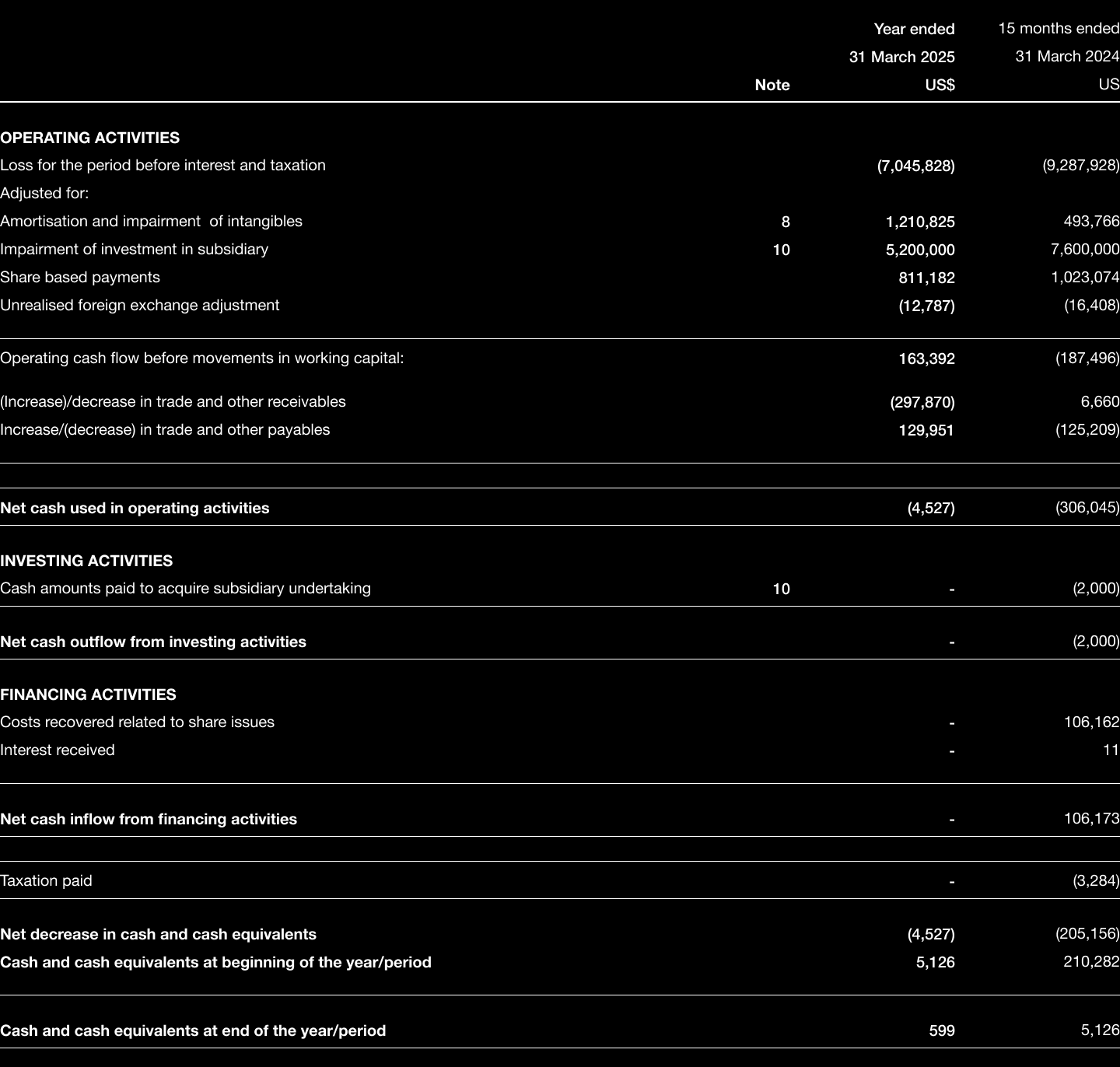

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 31 MARCH 2025

NARF INDUSTRIES PLC

PARENT COMPANY STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 31 MARCH 2025

NARF INDUSTRIES PLC

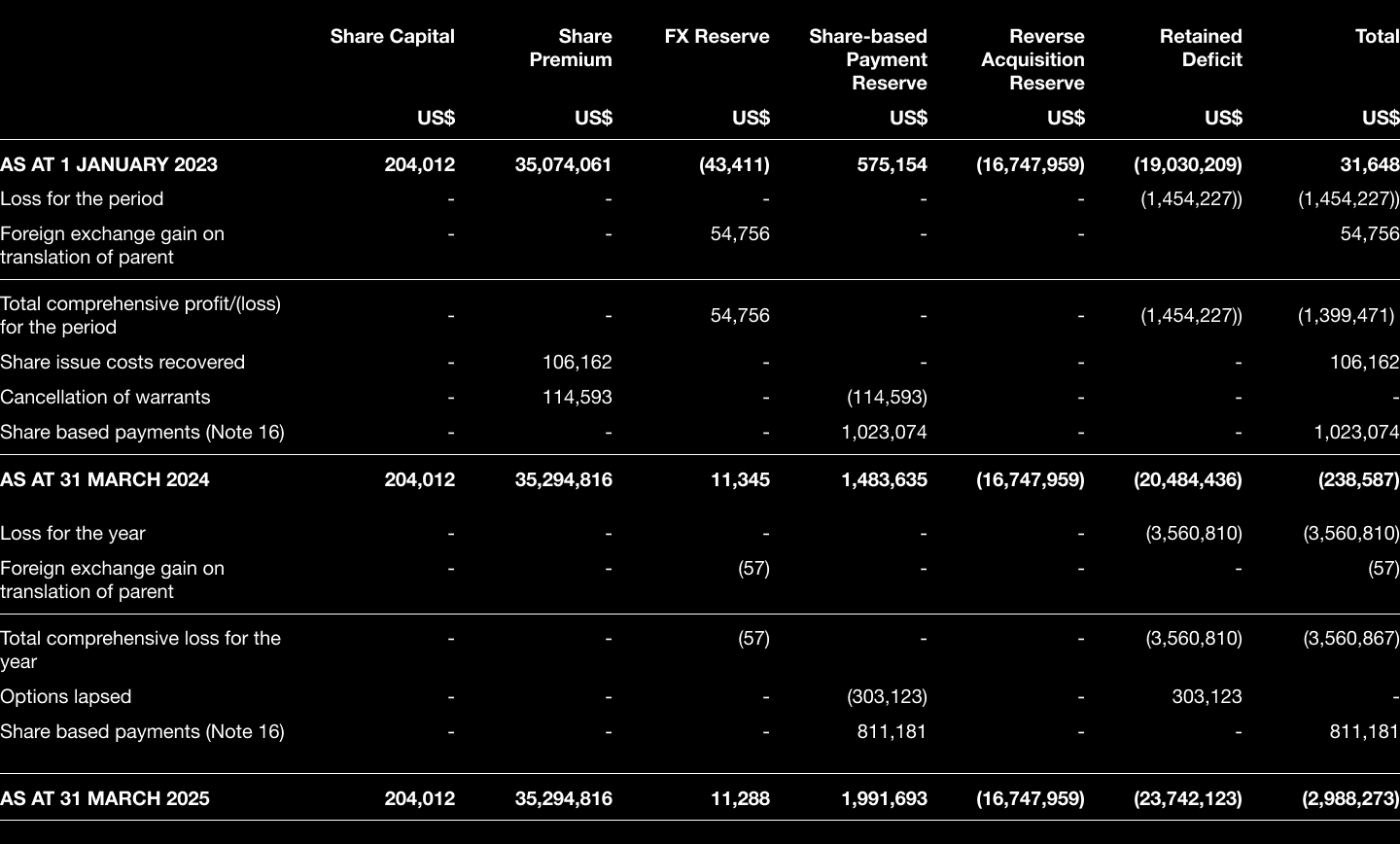

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 MARCH 2025

NARF INDUSTRIES PLC

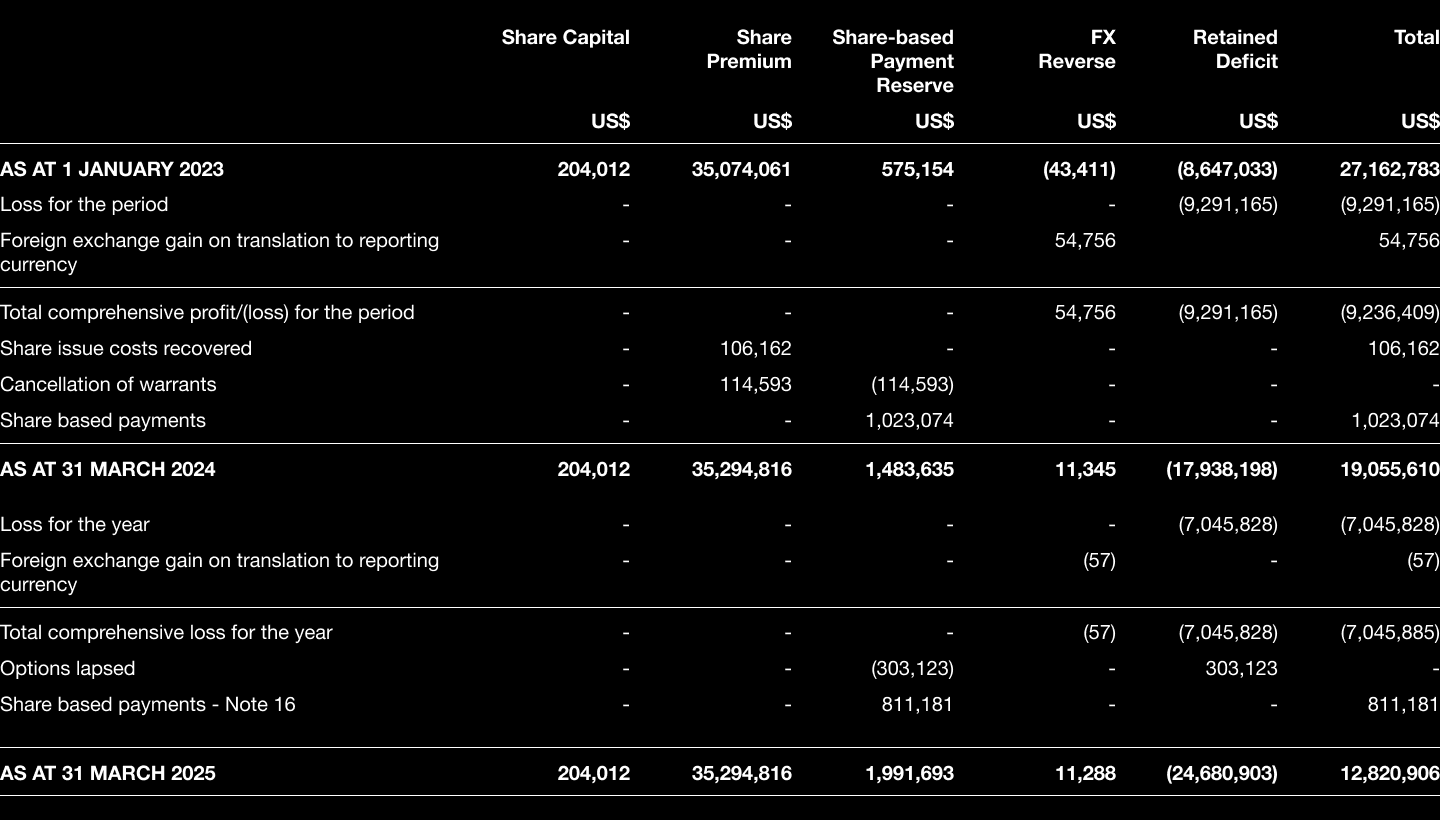

PARENT COMPANY STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 MARCH 2025

Share capital - the ordinary issued share capital of the Company.

Share premium - consideration less nominal value of issued shares and costs directly attributable to the issue of new shares.

Share based payment reserve - the value of equity settled share-based payments provided to past and present employees, including key management personnel, and third parties for services provided.

Foreign exchange reserve - a reserve arising on conversion of company balances in the functional currency of sterling and the reporting currency of US$.

Reverse acquisition reserve - the difference between the cost of acquiring the parent company and the fair value of the parent company's net assets on the acquisition date together with the deemed cost of listing.

Retained deficit - Cumulative net gains and losses recognised in the Statement of Comprehensive Income

NARF INDUSTRIES PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 MARCH 2025

1 GENERAL INFORMATION

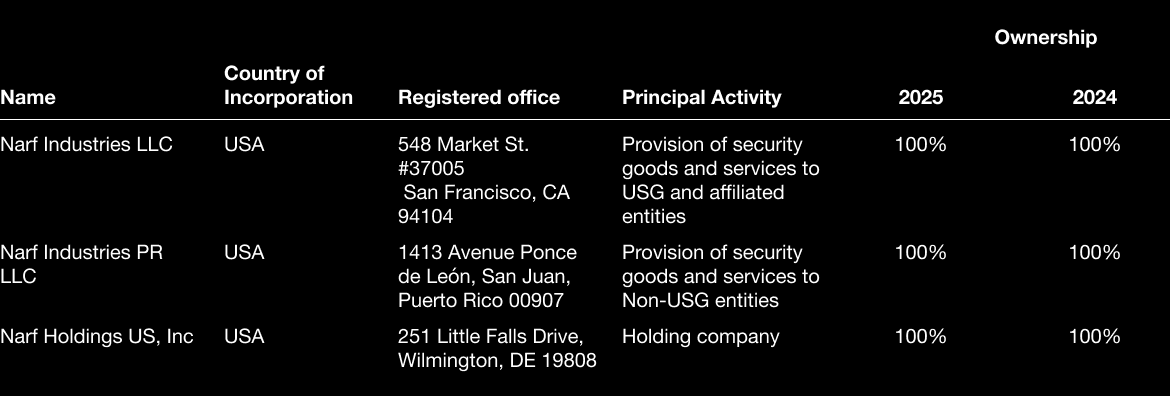

The principal activity of Narf Industries Plc (the "Company") and its subsidiaries (the "Group'') is the provision of research and software development services aimed at enhancing the cybersecurity measures of its US government agency clients. The subsidiaries consist of Narf Industries LLC, a California limited liability company, Narf Industries PR, LLC, a Puerto Rican limited liability company ("Narf US" or the "Operating Group") and Narf Holdings US, Inc. a Delaware corporation which was dormant throughout the period. The Company is the parent and sole shareholder of Narf Holdings US, Inc which, in turn, is the sole member of each entity in the Operating Group.

The Company is domiciled in the United Kingdom and incorporated and registered in England and Wales as a public limited company. The Company's registered office is 5 Fleet Place, London EC4M 7RD. The Company's registered number is 11701224.

2 ACCOUNTING POLICIES

2.1 Basis of preparation

The Consolidated Financial Statements of the Group have been prepared in accordance with UK-adopted international accounting standards.

The Financial Statements have been prepared under the historical cost convention unless otherwise stated. The principal accounting policies are set out below and have, unless otherwise stated, been applied consistently.

They have been prepared to reflect the acquisition of Narf Industries LLC and Narf Industries PR LLC via a reverse takeover on 15 March 2022, which resulted in the Company becoming the ultimate holding company of the Group.

The Financial Statements are prepared in US Dollar ("US$", "USD" or "$") and presented to the nearest dollar.

2.2 Consolidation and Acquisitions

The Financial Statements consolidate the financial information of the Company and companies controlled by the Group (its subsidiaries) at each reporting date following the reverse takeover on 15 March 2022.

In the consolidated statement of financial position, the share capital and share premium as at 31 March 2024 and 31 March 2025 is that of Narf Industries Plc with the reverse acquisition reserve representing the difference between the deemed cost of the acquisition and the net assets of Narf Industries plc at 15 March 2022. The consolidated statement of comprehensive income for the fifteen-month period ended 31 March 2024 and the year ended 31 March 2025 include the results of both the parent and the Operating Group throughout the period.

Control is achieved where the Company has the power to govern the financial and operating policies of an investee entity, has the rights to variable returns from its involvement with the investee entity and has the ability to use its power to affect its returns. The results of subsidiaries acquired or sold are included in the financial information from the effective date of acquisition or up to the effective date of disposal, as appropriate. Where necessary, adjustments are made to the results of acquired subsidiaries to bring their accounting policies into line with those used by the Group. All intra-Group transactions, balances, income and expenses are eliminated on consolidation. The financial statements of all Group companies are adjusted, where necessary, to ensure the use of consistent accounting policies.

The Group applies the acquisition method to account for any business combinations that fall within the scope of IFRS 3.

Acquisition-related costs are expensed as incurred.

2.3 Comparative information

The Parent Company extended its period end from 31 December 2023 to 31 March 2024. Accordingly, prior period information covers the fifteen-month period to 31 March 2024 and therefore is not directly comparable to the current 12-month period.

2.4 Going concern

The Directors believe the Company and the Group have sufficient resources to continue in operational existence for the foreseeable future and at least until 31 July 2026, being 12 months after the date these financial statements were issued. Therefore, the Directors have applied the going concern basis of accounting in preparing the financial statements.

The Group has current liabilities (primarily due to the existing line of credit ("LOC") from the CEO) which are greater than current assets at the reporting date and there is a deficit on shareholders' equity.

However, the Directors believe that the Group's existing contract backlog and cash flow management provides sufficient runway to enable it to continue through the next period to execute its medium-term strategy without new capital resources or significant reliance on near term additional contracts awards. Over the year to 31 March 2025, the Group demonstrated its ability to respond rapidly to adverse circumstances by reducing costs whilst accessing its LOC. Despite the significant setbacks in GS&S revenue the Group was able to deliver on existing contracts, keep up to date with payments to suppliers and win new business.

The Group recently extended the existing LOC provided by the Group's CEO through to July 2026, whilst revenues from existing contracts in place at the time of this report are sufficient to cover all overheads and to start repaying the LOC drawn down. The Group continues to closely manage its operational expenses and has demonstrated significant flexibility to adjust its resources and expenses in line with its contracted revenues.

The Board is also open to potential joint ventures should an attractive opportunity arise, but the work to reduce cash outgoings along with the extension of the LOC means the Board need only consider those opportunities which add significant value to the Group. The Board further notes the Company's potential to pursue an LSE market fundraise in the event this is deemed appropriate and market conditions allow.

The Directors believe the Group's plan is based on sound analysis, however, since the Group's plans, to a certain extent, are reliant on market conditions and/or third parties there remains a material uncertainty as to the Group's ability to remain a going concern.

2.5 Revenue Recognition

Substantially all of the Group's revenues derive from long-term contracts with US government agencies. The majority of contracts are fixed price with monthly or quarterly milestones with contractual payments due on completion of deliverables identified with those milestones. The contractual arrangements fall into four types:

Research where the principal asset transferred to the client are ideas about potential cybersecurity threats and source code to test those threats.

Infrastructure where the principal asset transferred is a test environment along with the ongoing maintenance of the ability to test various scenarios and meetings where the principal asset transferred is the intellectual input to those meetings.

Meetings-based where the contract specifies a requirement for Group employees to prepare for and attend meetings where they will share their expertise and provide insights to the meeting.

Cost plus where the Group receives a fee based on the hours worked on a project with reimbursement of travel and sub-contract costs.

The nature of the research and infrastructure contracts is such that the deliverables themselves are of little value to the customer. The main value of the contract to the customer is the inherent promise that the Group will continue to provide the ideas and support to allow the customer to enhance its understanding of cybersecurity threats and how to counter them. Given that the deliverables themselves have no inherent value, the Group takes the view that revenue from research and infrastructure contracts should be recognized over time based on progress towards a milestone. For meetings-based contracts revenue is recognized when the meetings occur, as this is the point at which an asset is transferred to the client. For cost plus contracts revenue is recognised based on the hours worked on that project up to the period end.

2.6 Segmental Reporting

The Group has two business sectors, GR&D and GS&S as described in the Strategic Direction section of this Annual Report. The revenues attributable to each business segment are detailed in the Statement of Comprehensive Income whilst an analysis of those costs attributable to each business segment is provided in Note 3.

2.7 Foreign currency translation

The financial information is presented in US Dollars, which is the Group's presentational and functional currency as substantially all of the Group's operational activities are undertaken in US Dollars. The Company's functional currency is Sterling. Sterling amounts recorded in the accounting records of the Company are converted using the year-end foreign exchange rate for the year end balances and the average foreign exchange rate for movements during the year.

Transactions in currencies other than the functional currency are recognised at the rates of exchange on the dates of the transactions. At each balance sheet date, monetary assets and liabilities are retranslated at the rates prevailing at the balance sheet date with differences recognised in the Statement of Comprehensive Income in the period in which they arise.

2.8 Cash and cash equivalents

Cash and cash equivalents comprise cash at hand and current and instant access deposit balances at banks.

2.9 Intangible assets

Intangible assets comprise non-physical assets comprising the cost of acquiring the licensing rights in relation to the commercialisation of TIGR that can be determined with reasonable certainty. Royalty payments due to the licensor upon future sales cannot be determined with any certainty and accordingly have not been included in cost.

The license is amortised over the useful life of the license, which is based on the term of that license agreement.

All intangible assets have been assessed by management for impairment. Management consider the assets for impairment by considering if any impairment indicators, such as those listed in IAS 38, are met and that if any are met, they assess the recoverable value of the asset, being the higher of the fair value less costs to sell and value in use, and then compare this to the carrying value of the asset.

2.10 Tangible fixed assets

Tangible assets comprise physical assets such as cars, office furniture and leasehold improvements which will benefit the Group over their useful life. Tangible fixed assets are being depreciated on a straight-line basis over their estimated useful lives as follows:

Cars 4 years

Office furniture & equipment 4 years

Leasehold improvements Life of the lease

2.11 Leased assets

Identification of leased assets

For any new contracts entered into, the Group considers whether a contract is, or contains a lease. A lease is defined as 'a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for over a year in exchange for consideration'. To apply this definition the Group assesses whether the contract meets two key evaluations which are whether:

i) the contract contains an identified asset, which is either explicitly identified in the contract or implicitly specified by being identified at the time the asset is made available to the Group

ii) the Group has the right to obtain substantially all of the economic benefits from use of the identified asset throughout the period of use, considering its rights within the defined scope of the contract the Group has the right to direct the use of the identified asset throughout the period of use.

The Group assesses whether it has the right to direct 'how and for what purpose' the asset is used throughout the period of use.

Measurement and recognition of leases

At lease commencement date, the Group recognises a right-of-use asset and a lease liability on the balance sheet. The right-of-use asset is measured at cost, which is made up of the initial measurement of the lease liability, any initial direct costs incurred by the Group, and any lease payments made in advance of the lease commencement date (net of any incentives received). The Group depreciates the right-of-use assets on a straight-line basis from the lease commencement date to the earlier of the end of the useful life of the right-of-use asset or the end of the lease term. The Group also assesses the right-of-use asset for impairment when such indicators exist. At the commencement date, the Group measures the lease liability at the present value of the lease payments unpaid at that date, discounted using the interest rate implicit in the lease if that rate is readily available or the Group's incremental borrowing rate. Subsequent to initial measurement, the liability will be reduced for payments made and increased for interest accrued.

2.12 Trade and other receivables

Trade receivables are amounts due from customers for goods or services rendered in the ordinary course of business. Trade receivables are initially recognised at the amount of consideration that is unconditional, i.e. fair value and subsequently measured at amortised cost using the effective interest method, less loss allowance. Prepayments and other receivables are stated at their nominal values.

Due to the short-term nature of the current receivables, their carrying amount is considered to be the same as their fair value.

2.13 Trade and other payables

Trade payables are recognised initially at their fair value and subsequently measured at amortised cost, less repayments.

2.14 Financial instruments

Initial recognition

A financial asset or financial liability is recognised in the Statement of Financial Position when it arises or when the Group becomes part of the contractual terms of the financial instrument.

Classification

Financial assets at amortised cost

The Group measures financial assets at amortised cost if both of the following conditions are met:

- the asset is held within a business model whose objective is to collect contractual cash flows; and

- the contractual terms of the financial asset generating cash flows at specified dates only pertain to capital and interest payments on the balance of the initial capital.

Financial assets which are measured at amortised cost, are measured using the Effective Interest Rate Method (EIR) and are subject to impairment. Gains and losses are recognised in profit or loss when the asset is derecognised, modified or impaired.

Financial liabilities at amortised cost

Financial liabilities measured at amortised cost using the effective interest rate method include current borrowings and trade and other payables that are short term in nature. Financial liabilities are derecognised if the Company's obligations specified in the contract expire or are discharged or cancelled.

Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the effective interest rate ("EIR"). The EIR amortisation is included as finance costs in profit or loss. Trade payables other payables are non-interest bearing and are stated at amortised cost using the effective interest method.

Derecognition

A financial asset is derecognised when:

- the rights to receive cash flows from the asset have expired, or

- the Company has transferred its rights to receive cash flows from the asset or has undertaken the commitment to fully pay the cash flows received without significant delay to a third party under an arrangement and has either (a) transferred substantially all the risks and the assets of the asset or (b) has neither transferred nor held substantially all the risks and estimates of the asset but has transferred the control of the asset.

Impairment

The Company recognises a provision for impairment for expected credit losses regarding all financial assets. Expected credit losses are based on the balance between all the payable contractual cash flows and all discounted cash flows that the Company expects to receive. Regarding trade receivables, the Company applies the IFRS 9 simplified approach in order to calculate expected credit losses. Therefore, at every reporting date, provision for losses regarding a financial instrument is measured at an amount equal to the expected credit losses over its lifetime without monitoring changes in credit risk. To measure expected credit losses, trade receivables and contract assets have been grouped based on shared risk characteristics.

2.15 Equity

Share capital is determined using the nominal value of shares that have been issued.

The Share premium account includes any premiums received on the initial issuing of the share capital. Any transaction costs associated with the issuing of shares are deducted from the Share premium account, net of any related income tax benefits.

Equity-settled share-based payments are credited to a "Share based payments reserve" within the Consolidated Statement of Financial Position and the Parent Statement of Financial Position as a component of equity until related options or warrants are exercised or lapse.

The share-based payment reserve comprises share warrants issued to service providers and options issued to employees under long-term incentive schemes. Both share options and warrants are measured at fair value at the date of issue and treated as a separate component of equity.

The Foreign exchange reserve includes all exchange differences arising from translating the net assets of the parent from sterling into US Dollars, being the presentational currency.

Members equity represents the combined interests of each member of Narf US and Narf PR prior to the reverse acquisition ("RTO").

The Reverse acquisition reserve relates to the costs associated with the acquisition of Narf Industries Plc. A reverse acquisition occurs if the entity that issues securities (the legal acquirer) is identified as the acquiree for accounting purposes and the entity whose equity interests are acquired (legal acquiree) is the acquirer for accounting purposes.

The reverse acquisition in a previous year did not constitute a business combination and was accounted for in accordance with IFRS 2 "Share-based Payments" and associated IFRIC guidance. Although the reverse acquisition was not a business combination, the Company has become a legal parent and is required to apply IFRS 10 and prepare consolidated financial statements.

The Directors have prepared these financial statements using the reverse acquisition methodology, but with the result that rather than recognising goodwill, the difference between the equity value given up by Narf US's former owners and the share of the fair value of the net assets gained by these former owners, is charged to the Consolidated Statement of Comprehensive Income as a share-based payment on reverse acquisition.

Retained earnings include all current and prior period results as disclosed in the income statement.

2.16 Foreign currency

For the purposes of the consolidated financial statements, the results and financial position of each Group company are expressed in US Dollars ("$"), which is the functional currency of all of the operating entities in the Group, excluding the Company, and the presentation currency for the consolidated financial statements.

Exchange differences are recognised in the Statement of Comprehensive Income in the period in which they arise other than those arising on conversion of the Company's Statement of Financial Position on consolidation which are recognised as a foreign exchange reserve.

2.17 Earnings per share

Basic earnings per share is calculated by dividing:

The Group loss attributable to owners of the Company, excluding any costs of servicing equity other than ordinary shares by the weighted average number of ordinary shares outstanding during the financial period.

As the Group is currently loss making, none of the options or warrants in issue are dilutive to the basic earnings per share figure.

2.18 Share-based payments

The Parent Company has issued options to Directors and Group employees under long-term incentive arrangements.

Equity-settled share-based payments are measured at fair value (excluding the effect of non-market based vesting conditions) at the date of grant. The fair value so determined is expensed on a straight-line basis over the vesting period, based on the Parent Company's estimate of the number of shares that will eventually vest and adjusted for the effect of non-market based vesting conditions.

Fair value is measured using the Black Scholes pricing model. The key assumptions used in the model have been adjusted, based on management's best estimate, for the effects of non-transferability, exercise restrictions and behavioural considerations.

At the time of the RTO, Narf US had entered into agreements with a number of key employees whereby they were entitled to an interest in Narf Industries LLC. Ahead of the RTO those employees entered into redemption agreements, so as to release Narf US from the obligation to provide such an interest. As at 31 March 2024 two former employees were owed a total of $335,435 under these redemption agreements. During the year $311,250 was settled through the issue of warrants and $20,000 was settled in cash.

2.19 Taxation

The Parent Company is subject to taxes in the United Kingdom tax jurisdiction and, to the extent there are look through profits in the Operating Group, is also subject to taxes in the United States. Substantially all revenue related operations are conducted by Narf Industries LLC. Both operating subsidiaries are limited liability companies taxed as partnerships for US federal taxes. As partnerships, neither operating subsidiary is subject to US federal income tax and the federal tax effect of those activities now accrue to Narf Holdings, Inc, the sole member. Narf Industries LLC is also subject to a nominal California franchise tax, whilst Narf Industries PR LLC is subject to the Government of the Commonwealth of Puerto income tax rate of 4%. The Operating Group currently has substantial tax losses attributable to the Parent Company, for which no deferred tax has been recognised and accordingly, differences between Narf US's taxable income per IFRS and the basis used for tax reporting have not given rise to any deferred tax assets or liabilities.

Taxable losses of the Parent Company from its activities in the United Kingdom and that inure to the Parent Company from the two members of the Operating Group as their sole partner differ from losses for the Parent Company as reported in the accompanying consolidated income statement because it excludes items of income and expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Parent Company's liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the balance sheet date.

Deferred tax is recognised on differences between the carrying amounts of assets and liabilities in the accompanying parent company financial statements and the corresponding tax bases used in the computation of taxable profit and is accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognised for all taxable temporary differences and deferred tax assets are recognised to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilised. Such assets and liabilities are not recognised if the temporary difference arises from initial recognition of goodwill or from the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit.

Deferred tax liabilities are recognised for taxable temporary differences arising on investments in subsidiaries and associates, and interests in joint ventures, except where the Parent Company is able to control the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at each balance sheet date and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax is calculated at the tax rates that are expected to apply in the period when the liability is settled, or the asset realised. Deferred tax is charged or credited to profit or loss, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the Parent Company intends to settle its current tax assets and liabilities on a net basis.

2.20 Critical accounting judgements and key sources of estimation uncertainty

In the process of applying the entity's accounting policies, management makes estimates and assumptions that have an effect on the amounts recognised in the financial information. Although these estimates are based on management's best knowledge of current events and actions, actual results may ultimately differ from those estimates. The Directors consider that the following judgements are critical to an understanding of these accounts:

Licenses

The Parent Company was historically granted certain licenses relating to the commercialisation of cybersecurity software which potentially could be key to the future business strategy. The license was granted by SRI International, under an agreement which became effective on 15 March 2022, for a combination of cash, shares and a royalty equal to 7.5% of future revenues deriving from the license. The Directors recognised the fair value of the license on acquisition as being the cash paid plus the market value of shares issued to SRI International.

The value of the license has been assessed by management for impairment. Management considers the asset value for impairment by considering if any impairment indicators, such as those per IAS 38, are met and that if any are met, they assess the recoverable value of the license, being the higher of the Fair value less costs to sell and Value in use, and then compare this to the carrying value of the license. Management has made the decision to fully impair the license because a feasibility study is being considered and until this is completed, any assessment of Value in Use is considered too subjective to quantify. Further details are provided in Note 8.

Impairment of Narf US

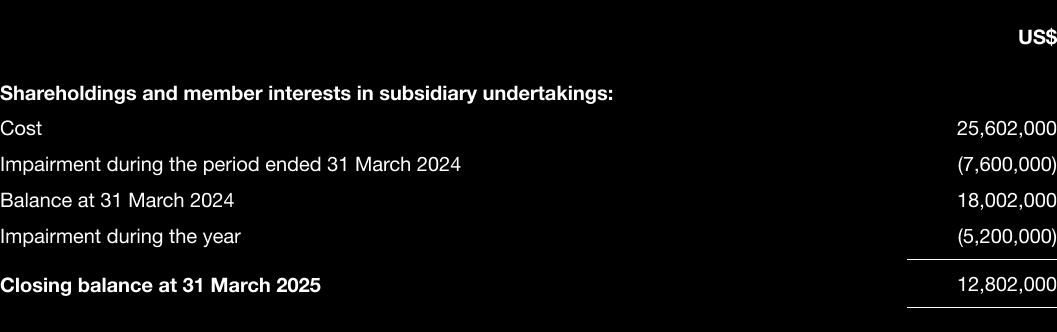

The Parent Company Statement of Financial Position includes the investment in Narf US at cost less impairment. The Directors undertook an impairment review as at 31 December 2024. At that time, the Directors took the view that the investment should be written down further in light of the GS &S revenue impact. Management increased the impairment provision by $5.2 million to $12.8 million which reflected the delay in expected future cash flows and the significant reduction in the share price. A further impairment review was conducted ahead of the issue of these financial statements and no further impairment was deemed appropriate. This review involves judgements about potential future cash flows which are highly subjective and subject to matters outside the control of the Directors.

Segmental Reporting

Note 3 seeks to analyse the contribution of each business segment to the profitability of the Group. The allocation of costs includes the costs of some employees who work on both business segments which requires judgements as to the allocation of resources. Management have not sought to allocate costs related to the time of the CEO because he has agreed to waive any remuneration until his loan is repaid.

Share Based Payments

Equity-settled share-based payments are measured at fair value. Fair value is measured using the Black Scholes pricing model. The key assumptions used in the model have been adjusted, based on management's best estimate, for the effects of non-transferability, exercise restrictions and behavioural considerations. The fair value also makes certain assumptions about whether non-market vesting conditions will be met and such assumptions are highly subjective.

2.20 Critical accounting judgements and key sources of estimation uncertainty

Revenue recognition

The Group's revenues arise from contracts which generally have monthly or quarterly payment milestones. Some of these contracts span more than one accounting period and some are based on provisional calculations of indirect costs, which are subject to independent audit and revision. The Group generally recognises revenue based on milestones that have been met, the labour hours incurred or the amount of time that has progressed towards a milestone which has been met post period-end.

Nonetheless there is some uncertainty at each milestone date as to the extent to which additional work may have been completed and the extent to which the contracted amount attributable to each milestone represents a fair proportion of the overall contract. Management rely on the output method to allocate revenue between accounting periods.

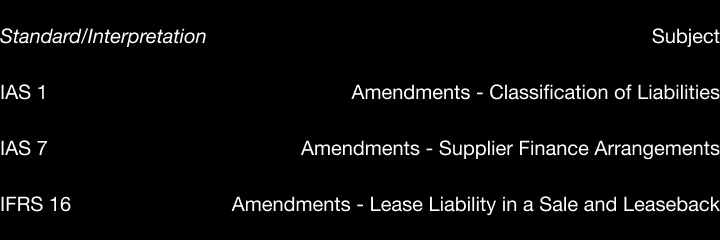

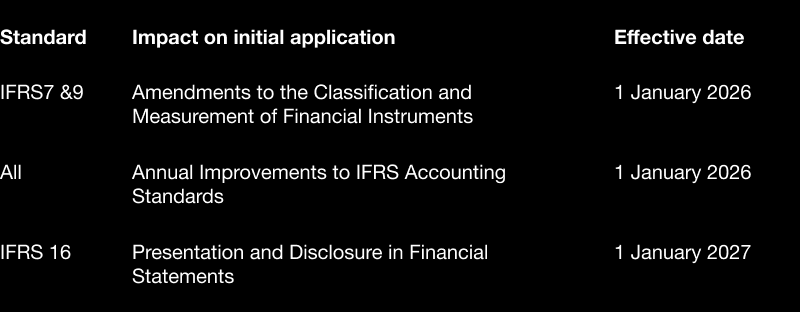

2.21 Standards, amendments and interpretations to existing standards that are not yet effective

New standards, amendments to standards and interpretations:

The Company has adopted all of the new and revised Standards and Interpretations that are relevant to their operations and effective for accounting periods beginning 1 April 2024. The Company has not adopted any standards or interpretations in advance of their required implementation dates.

The following Standards and Interpretations have become effective and, if relevant, have been adopted in these financial statements. No other Standards or Interpretations have been adopted early in these financial statements.

The new standards have not had a material impact on these consolidated financial statements.

Standards not yet applied

At the date of authorisation of these financial statements, the following relevant Standards and Interpretations, which have not been applied in these financial statements, were in issue but not yet effective.

The Group intends to adopt these new and amended standards and interpretations, if applicable, when they become effective.

2.22 Financial Risk Management Objectives and Policies

The Group does not enter into any forward exchange rate contracts nor does it have any other market risks apart from the Sterling assets held by the Parent Company which are matched by Sterling liabilities.

The main financial risks arising from the Group's activities are interest rate risk, credit risk, liquidity risk and capital risk management. Further details on the risk disclosures can be found in Notes 19 and 20.

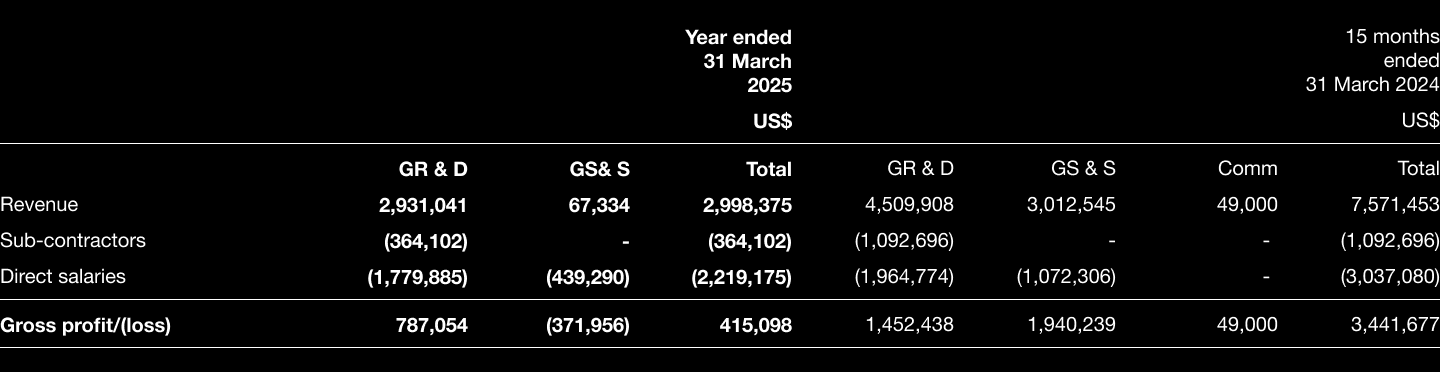

3. REVENUE AND SEGMENTAL REPORTING

The Group records contract revenue in accordance with IFRS 15 Revenue from Contracts with Customers, which requires that revenue be recorded over time as/when performance obligations within contracts are performed/delivered. Whilst some performance obligations are defined within the Group's contracts, management considers that the main asset transferred to the customers over the term of the contract is the implied promise that the customer will have access to Group employees throughout the duration of the contract. The customer is expecting that those employees will be able to come up with ideas, explaining outputs from the software developed and generally push the boundaries to understand how to develop what may start as a concept into something that has commercial value. The Group invoices customers based on a billing schedule contained within each contract. The Group considers trade and other receivables to be fully collectible as it has no history of non-payment; accordingly, no allowance for doubtful accounts has been recorded at either period end. Costs incurred to obtain contracts are expensed as incurred and losses on contracts are recognised in the period when determined. The Group sometimes warrants that its deliverables will perform within parameters contained in the statements of work referenced in the contracts.

Revenue for performance obligations is generally recognised as each performance obligation is completed and, to the extent applicable, delivered - an output measurement. Where a performance obligation crosses a period end, revenue for that performance allocation is pro-rated on a time expired basis and allocated proportionately to the relevant period.

As performance obligations are completed and delivered, invoices are issued to customers and the debtor recorded in the Trade Accounts Receivables, which represents a conditional right to consideration, which generally becomes an unconditional right on payment. There were no amounts invoiced that were subsequently challenged as being in excess of completed performance obligations as at 31 March, 2025 or 31 March, 2024. To the extent that the measurement of outputs suggests that a future milestone has been met in part, a debtor is recorded in the caption Prepayments and Accrued Income.

During the period under review the Group established the two separate business segments of GR & D and GS & S, with each segment having a business head. The prior year numbers have been restated to reflect the different business segments.

Based on the above categories, disaggregated contract revenues and their related costs as follow

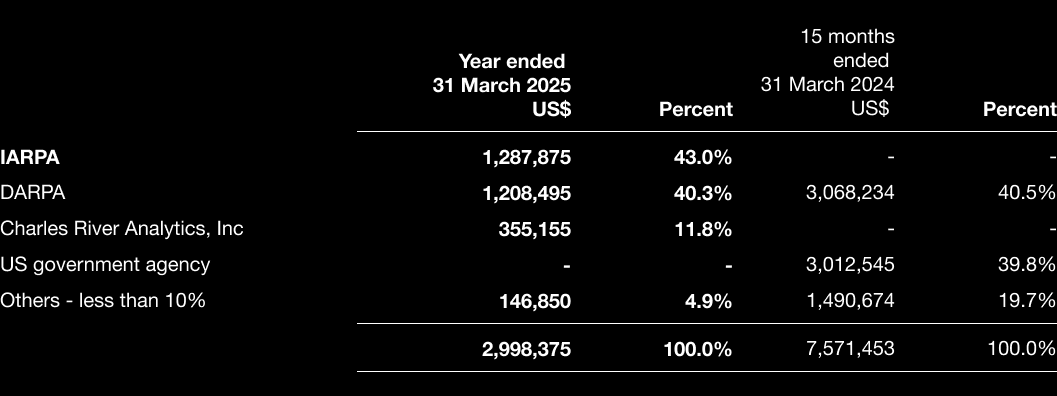

Customers comprising 10% or more of Contract Revenue were as follows:

For contractual reasons, the Company may not disclose the name of the US government procurement agency or the agencies for which this entity is pass-through. DARPA stands for Defense Advanced Research Projects Agency, a US government research and development organisation. IARPA stands for Intelligence Advanced Research Projects Activity, another US government research and development organisation.

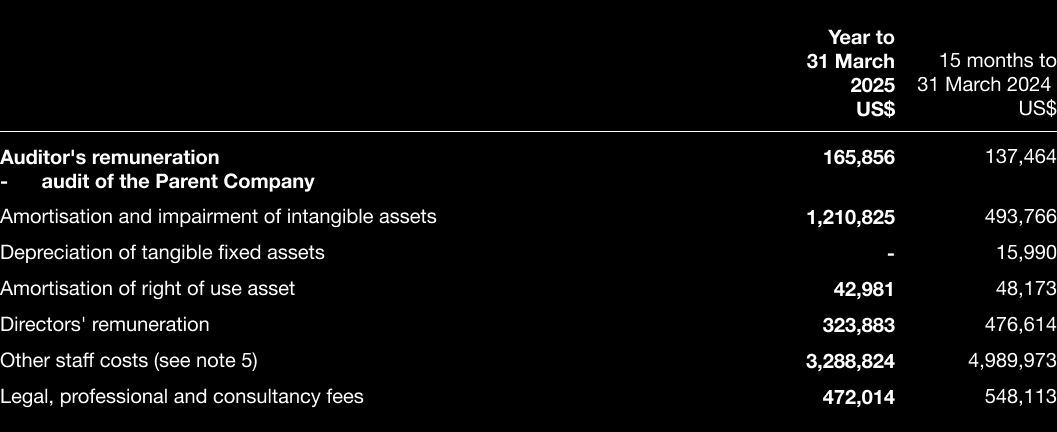

4. OPERATING LOSS

This is stated after charging:

5. DIRECTORS AND STAFF COSTS

The average number of persons employed by the Group, including Directors, was:

Remuneration, other benefits supplied and social security costs to the directors and staff during the period was as follows:

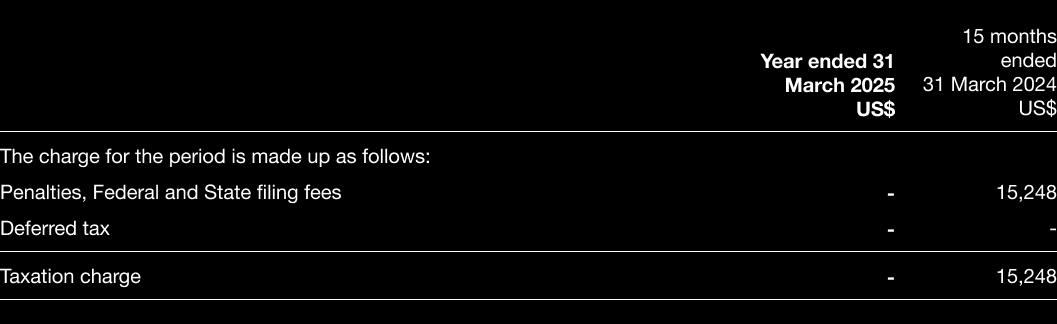

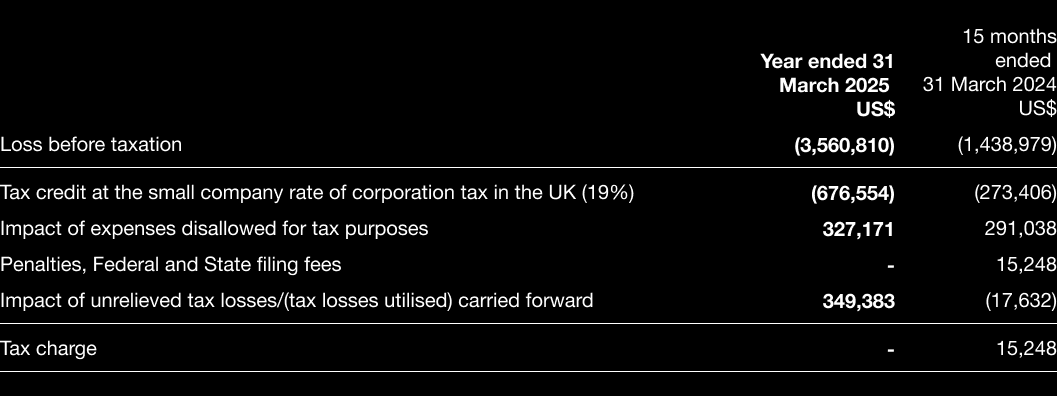

6. TAXATION

A reconciliation of the tax charge / credit appearing in the income statement to the tax that would result from applying the standard rate of tax to the results for the period is:

Estimated tax losses of $8.2 million (2024: $6.1 million) are available for relief against future UK profits and estimated tax losses of $2.9 million (2024: $1.2 million) are available for relief against future US profits. No related deferred tax asset has been provided for in the accounts based on the uncertainty as to when profits will be generated against which to relieve said asset. The amount of the deferred tax asset not recognised in relation to losses for the Group is $2.7 million (2024: $1.4 million) and for the Company $2.1 million (2024: $1.1 million).

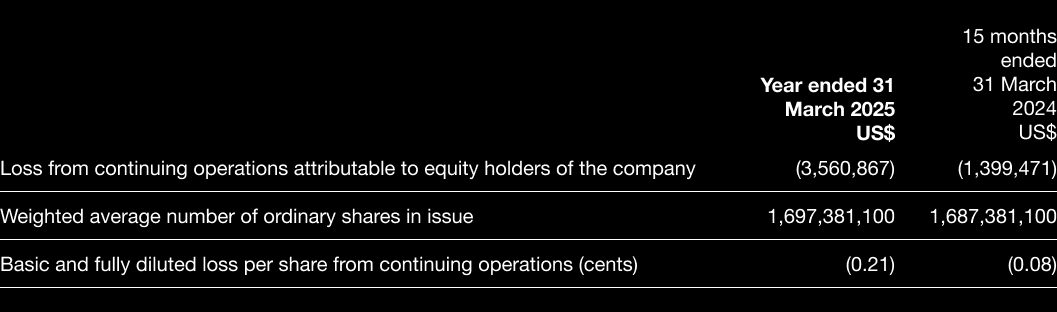

7. EARNINGS AND DILUTED EARNINGS PER SHARE

Basic earnings per share is calculated by dividing the loss attributable to equity holders of the Company by the weighted average number of ordinary shares in issue during the period.

No dilution has been applied in respect of the options outstanding at the period end because the Group is loss making.

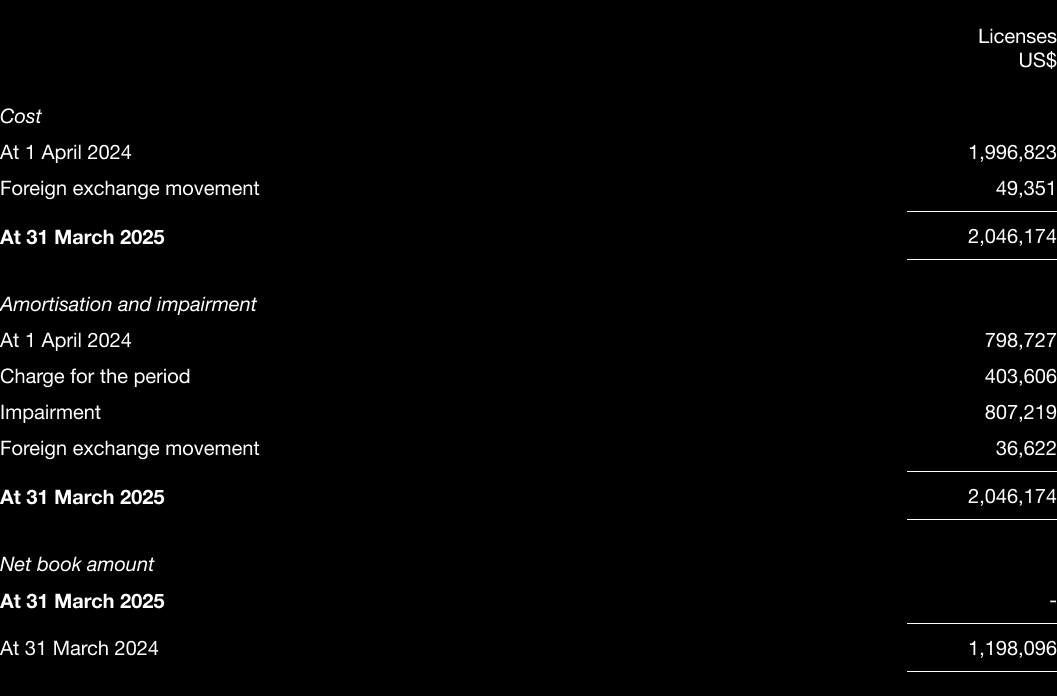

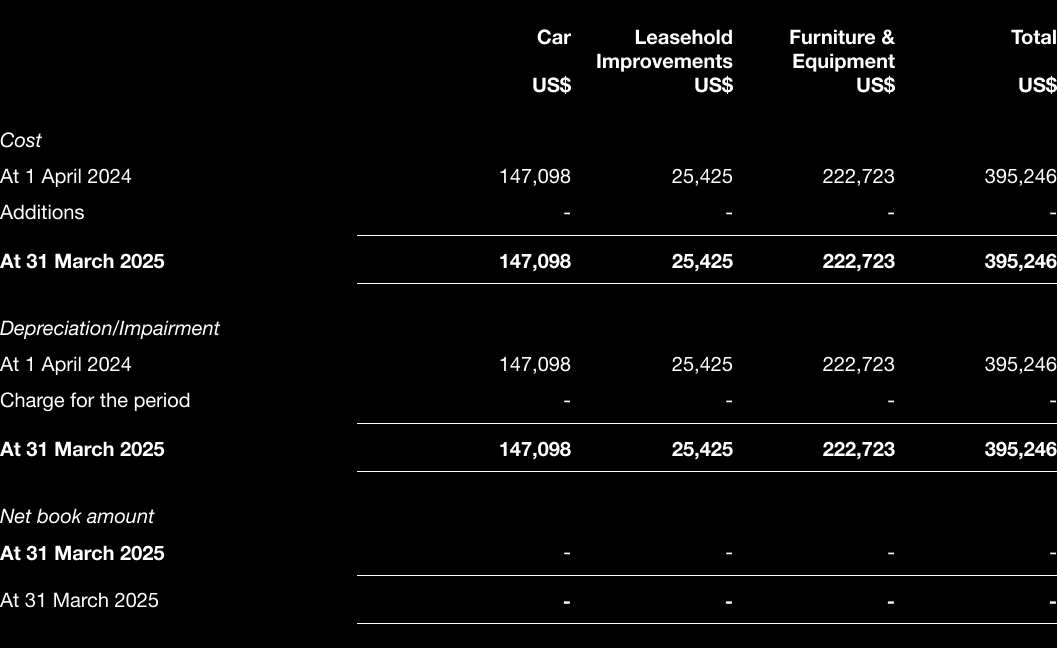

8. INTANGIBLE ASSETS - GROUP AND PARENT COMPANY

Amortisation ad impairment of licenses is charged to the Income statement in the period to which it relates and disclosed within "Depreciation, amortisation and impairment of fixed assets".

Depreciation of tangible assets is charged to the Income statement in the period to which it relates and disclosed within "Depreciation, amortisation and impairment of fixed assets". The car was sold to the CEO after the year end (see note 22).

10. INVESTMENTS IN SUBSIDIARY UNDERTAKINGS - PARENT COMPANY

Investments in subsidiary undertakings are valued at cost less the Directors' impairment assessment which reflects changes in the business plan of the subsidiaries since the reverse takeover.

Principal subsidiaries

The group's subsidiaries at 31 March 2025 are set out below. Two of the subsidiaries are LLCs, which have no issued share capital and accordingly the proportion of ownership interests held equals the voting rights held by the group. The country of incorporation or registration is also their principal place of business.

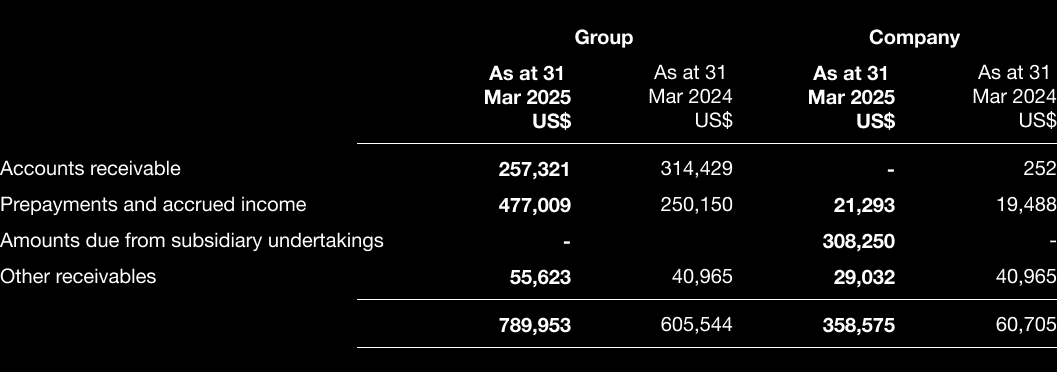

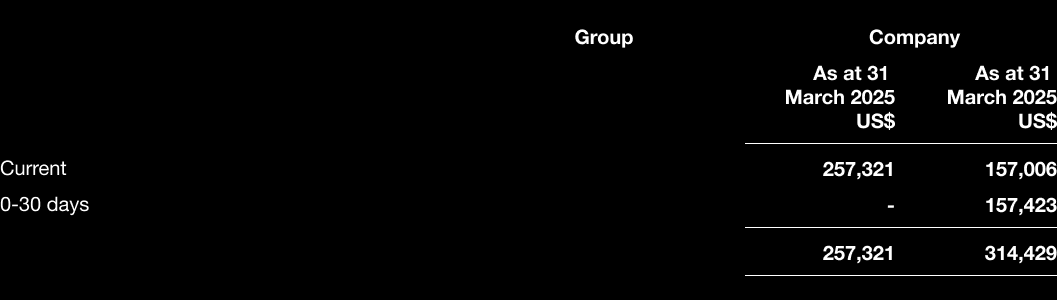

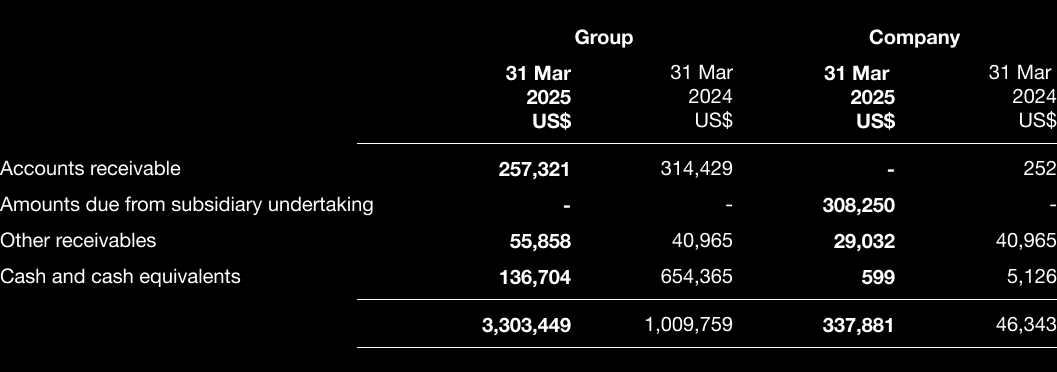

11. TRADE AND OTHER RECEIVABLES - GROUP AND PARENT COMPANY

The Directors consider that the carrying value amount of trade and other receivables approximates to their fair value.

11. TRADE AND OTHER RECEIVABLES - GROUP AND PARENT COMPANY (CONTINUED)

Ageing analysis

The following presents an ageing analysis of Accounts Receivable:

The Group considers trade and other receivables to be fully collectible; accordingly, no bad debt provision or expenses have been recorded in either financial period ending 31 March 2025 and 31 March 2024 respectively and all amounts listed in Accounts Receivable were received post period-end.

12. CASH AND CASH EQUIVALENTS - GROUP AND PARENT COMPANY

Cash at bank comprises balances held by the Company in current bank accounts, instant access deposit accounts and electronic wallets. The carrying value of these approximates to their fair value. The majority of cash is held in a bank with a BBB+ credit rating.

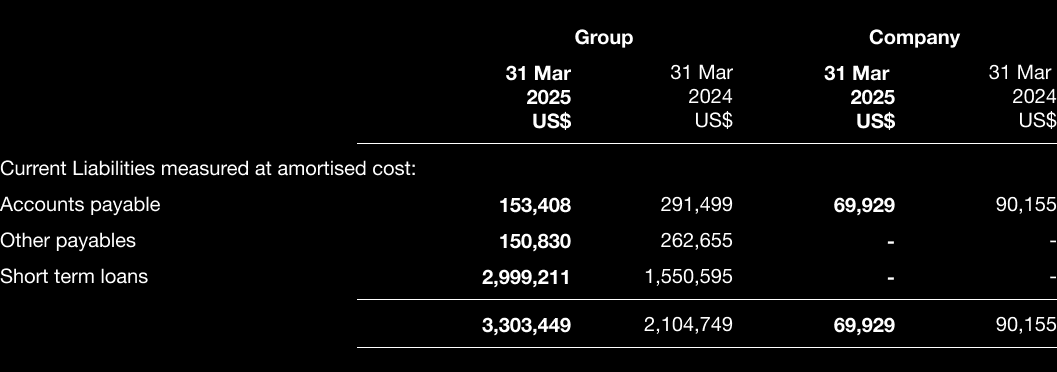

13. TRADE AND OTHER PAYABLES - GROUP AND PARENT COMPANY

Trade payables and accruals principally comprise amounts outstanding for trade purchases and continuing costs. The Directors consider that the carrying value amount of trade and other payables approximates to their fair value. Refer to Note 18.

The Loan from Director and Chief Executive Officer represents advances to the Group (plus accrued interest of $169,461) for working capital purposes from Steve Bassi, CEO (see Note 22). The loan was, until 28 June 2024, part of a $2 million credit facility accruing simple interest daily at the US Federal short term 1 year interest rate (4.86% at 11 April, 2023). On 28 June 2024 the credit facility was increased to $2.5 million and the term extended to 31 July 2025, with the same rate of interest. On 29 December 2024 the credit facility was increased to $3 million. Effective 1 August 2025 the credit facility was extended until 31 July 2026. A portion or all of the note may be repaid early without penalty and the Director may request the Group to pay amounts when working capital exceeds $500,000 at the end of any given month. This credit facility is being presented without any discount to account for time as the facility may be partially or fully repaid prior to the due date of 31 July, 2026.

14. SHARE CAPITAL / SHARE PREMIUM - GROUP AND PARENT COMPANY

The Company has only one class of share. All ordinary shares of 0.1p each ("Shares") have equal voting rights and rank pari passu for the distribution of dividends and repayment of capital. As at 31 March 2025 and 31 March 2024 the Company's issued and outstanding capital structure comprised 1,697,381,100 shares and there were no other securities in issue and outstanding.

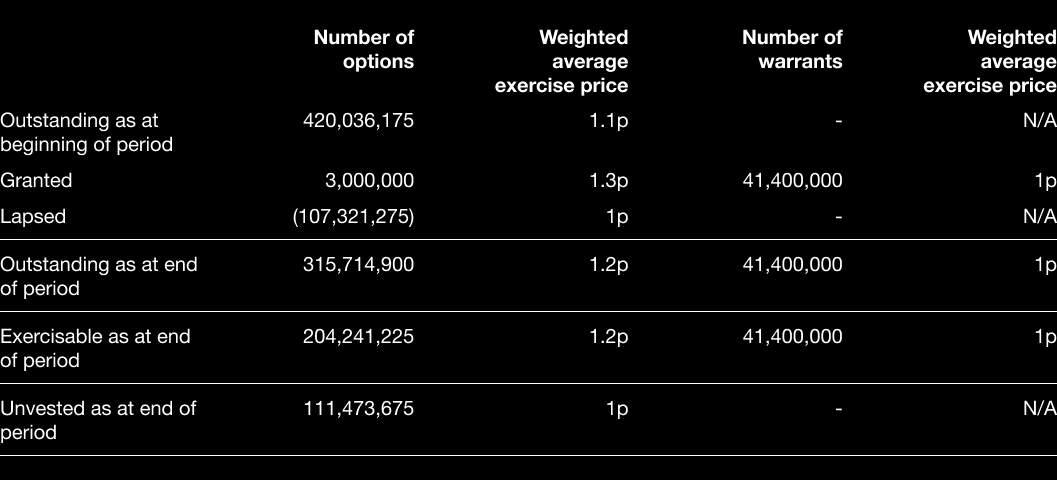

At 31 March 2025 the Company had 202.8 million options outstanding and 51.6 million warrants outstanding (see note 15)

15. SHARE BASED PAYMENT RESERVE- GROUP AND PARENT COMPANY

Details of the warrants that were outstanding at 31 March 2025 are as follows:

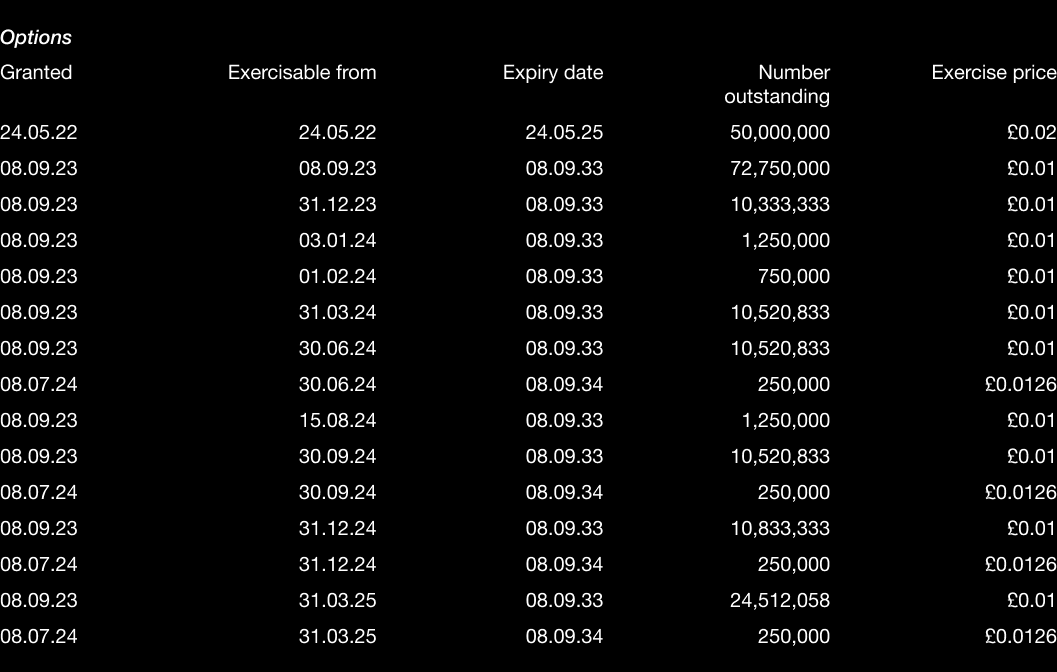

Details of the options that were outstanding at 31 March 2025 are set out below:

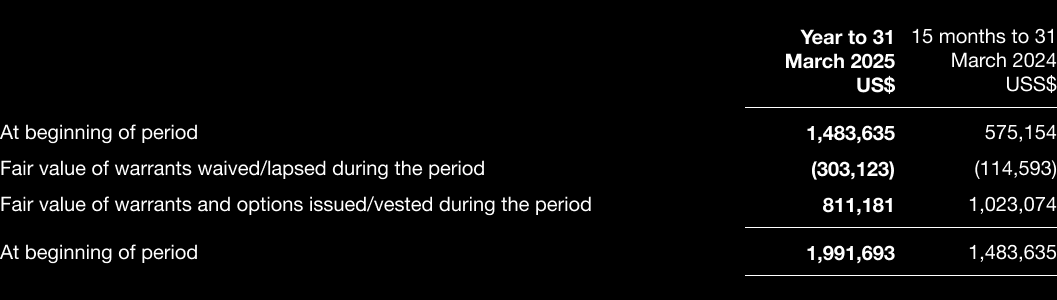

An additional 109.4 million £0.01 options and 2 million £0.0126 options had been granted at the period end which are subject to vesting conditions which hadn't been met at 31 March 2025 but are expected to be met in the future. The movements in the share-based payment reserve are as follows:

Of the amount credited to share based payment reserve $499,831 (15 months to 31 March, 2024: $1,023,074) related to options issued for services provided and therefore resulted in a charge to the Statement of Comprehensive Income and $311,250 (15 months to 31 March, 2024 $nil) related to an amount due to a former employee that had previously been accrued for.

A share-based payment credit of $303,123 (fifteen months to 31 March 2024 $114,593) was recognised during the year on options that lapsed due to employees leaving or vesting conditions not being met.

The estimated fair value of the options granted in September 2023 and July 2024 and the warrants granted in August 2024 were calculated by applying the Black-Scholes option pricing model. The assumptions used in the calculation were as set out below:

*The expected volatility was calculated using historical 360-day volatility of the share price of Narf Industries plc for the year to 31 March 2023 (since the shares were suspended for a significant part of the period from 1 April 2023 to the date of grant).

The movements in share options and share warrants are as follows:

16. LEASES - GROUP

As further discussed in Note 20, the Group has a lease agreement in relation to their office in California which expires on 1 December 2025, including minimum rental payments of $5,000 per month. As this lease has a term of one year it is considered a short-term lease under the requirements of IFRS 16 - Leases and the monthly rent is being accounted for in the Statement of Comprehensive Income as it becomes due.

Commitments payable in respect of short-term leases comprise:

Effective 1 June 2023, the Group entered into a lease agreement in relation to their office in California which expired on 31 December 2024, including minimum rental payments of $5,000 per month. As this lease had a term of over one year it has been accounted for in accordance with the provisions of IFRS 16

- Leases with a right of use asset recognised in the Statement of Financial Position and an offsetting lease liability.

Additional information on the right of use asset is as follows:

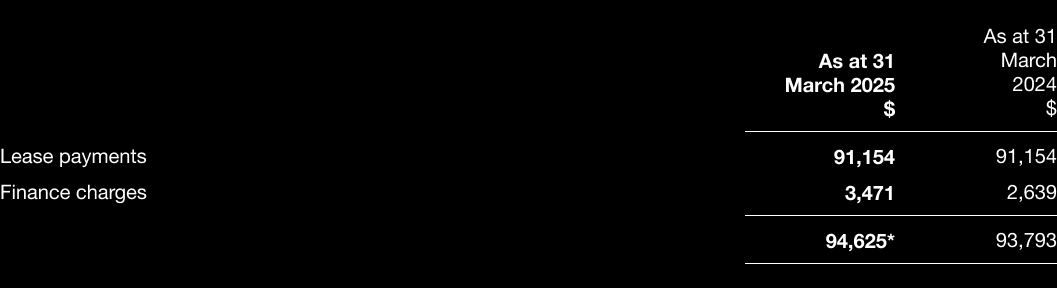

The net present value of lease liabilities accounted for under IFRS 16 are all due within 1 year and comprise

* The lease liability relates to a former right of use asset where the lease has ended but the Group has not settled the lease payments due.

17. CONTINGENT LIABILITIES

There were no contingent liabilities at 31 March 2025 (31 March 2024: £nil).

18. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT

The Group's financial instruments comprise primarily cash and various items such as trade debtors and trade payables which arise directly from operations. The main purpose of these financial instruments is to provide working capital for the Group's operations. The Group does not utilise complex financial instruments or hedging mechanisms.

Financial assets by category

The categories of financial assets are as follows:

Financial liabilities by category

The categories of financial liabilities are as follows:

All amounts owed by the Parent Company and the Group are short term and payable in 0 to 3 months, apart from the short-term loan which is disclosed in Notes 13 and 20.. The short-term loan facility has been extended to 30 June 2026 but is repayable on demand under certain circumstances.

Credit risk

Credit risk is the risk that an amount owed to the Parent Company or the Group will not be settled as a result of the failure of the counterparty. Credit risk is considered to be minimal as accounts receivable are due from US government agencies with no history of non-payment, other receivables represent VAT due from the UK government or payroll taxes recoverable from the IRS and cash is held in high street banks with most of the deposits protected.

The maximum exposure to credit risk at the reporting date by class of financial asset was:

Foreign exchange risk

The Group operates principally in the USA with income and operating costs possibly arising in US Dollars. The majority of the operating revenues and costs are incurred in US Dollars although there are a number of Sterling costs incurred by the Parent Company in relation to the costs of maintaining a listing. The Company does not hedge potential future income or costs, since the existence, quantum and timing of such transactions cannot be accurately predicted. The Company's and therefore the Group's exposure to non- US Dollar assets and liabilities is detailed below.

Given the insignificant foreign exchange exposure, management do not believe that sensitivity analysis would provide any meaningful information to readers of these accounts.

Interest rate risk

The only Parent Company or Group's asset or liability that is subject to any material interest rate risk is the loan from the CEO which has a variable interest rate. All deposits are placed with main clearing banks with minimal amounts attracting interest.

Liquidity risk

The Parent Company and the Group seek to maintain adequate bank balances to meet those financial liabilities that are payable in the short term (between 0 to 3 months) but has access to the CEO's credit facility in the event of a shortfall.

19. CAPITAL MANAGEMENT

The Group manages its capital with a view to ensuring that it will be able to continue as a going concern while maximising the return to shareholders through the optimisation of the balance between debt and equity. The Group utilizes options on its shares to seek to incentivize the Directors and Group employees to remain loyal and meet strategic goals which will add shareholder value.

The capital structure of the Group as at 31 March, 2025 consisted of negative equity attributable to the equity holders of the Group, totalling $2,988,273 (2024: $238,587) bolstered by working capital advances from an officer and shareholder of $2,999,211 (2024: $1,550,595) (see Notes 13 and 20).

The Group reviews the capital structure on an on-going basis. As part of this review, the directors consider the cost of capital and the risks associated with each class of capital. The Group will balance its overall capital structure through new share issues or potentially through the issue of convertible debt instruments. There are no plans to pay dividends for the foreseeable future.

20. RELATED PARTY TRANSACTIONS

The compensation payable to Key Management personnel, who comprise the Directors, comprised $113,000 in amounts payable by the Group together with the fair value of options issued in respect of services to the Group. Full details of the compensation for each Director are provided in the Directors' Remuneration Report. At year-end, an amount of $14,853 was due to a former director and officer in respect of Directors remuneration.

Included in Trade and Other Payables in the accompanying Consolidated Statement of Financial Position are balances of $16,300 and $16,000 at 31 March, 2025 and 31 March, 2024 respectively, related to an office operating lease agreement with a term of one year between the Group and an entity in which Steve Bassi is an owner. Included in Trade and Other Payables in the accompanying Consolidated Statement of Financial Position are balances of $94,625 and $93,793 at 31 March, 2025 and 31 March, 2024 respectively, related to an office operating lease agreement which had an original term of over one year between the Group and an entity in which Steve Bassi is an owner. The amount remains unpaid. The amount reported as a Right of Use Asset in the Consolidated Statement of Financial Position of $nil (2024: $42,981) is a right over an asset owned by that same entity.

Included in Administrative Expenses on the accompanying Consolidated Statement of Comprehensive income is US$300 (2024: US$24,000) in operating lease expense, $48,173 (2024: $42,981) in amortisation of right of use asset and $832 (2024: $2,639) of lease interest relating to leases entered into with that related entity.

As further discussed in Note 13, a Director and CEO made loans to the Company which at period end totalled $2,999,211 including accrued interest (2022: $1,550,595). The amounts represent a drawdown on a $3 million credit facility with a variable rate of interest.

21. PRIOR YEAR ADJUSTMENT

During the preparation of these financial statements, it was noted that the share-based payment charge was classed as an expense in Narf Industries PLC company accounts in the prior period. This was a classification error as the charge is borne by the group's subsidiaries as employer of the staff holding share options. The share-based payment charge then adjusts the intercompany management charge used to recharge expenses.

Accordingly, there is no adjustment to the results as previously reported but references to share based payments in the PLC company cash flow statement have been corrected to reflect the expense as a management charge rather than a share based payment.

22. EVENTS SUBSEQUENT TO YEAR END

Effective 1 August the loan facility of $3 million provided by the CEO was extended to 31 July 2026. Under this agreement the Group's car (see Note 9) was transferred to the CEO with a profit on disposal to the Group of $30,000.

23. CONTROL

In the opinion of the Directors there is no single ultimate controlling party.

This information is provided by RNS, the news service of the London Stock Exchange. RNS is approved by the Financial Conduct Authority to act as a Primary Information Provider in the United Kingdom. Terms and conditions relating to the use and distribution of this information may apply. For further information, please contact rns@lseg.com or visit www.rns.com.RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.